The Current Growth of the Private Credit Market and Its Implications for Investors

The private credit market is witnessing a substantial expansion, and investors need to take note of its implications. This market, which encompasses lending and borrowing outside of mainstream banks and capital markets, has been growing rapidly due to regulatory shifts and the rising demand for alternative financing. By understanding the significance of this growth, investors can make informed decisions and capitalize on the opportunities presented by the private credit market.

Including private credit and private equity in portfolios offers several benefits. These investments may offer higher returns compared to traditional asset classes, making them attractive for yield-seeking investors. Active management in private equity can lead to alpha generation through strategic investments and growth initiatives. Moreover, private credit and private equity typically exhibit low correlation with public equities and bonds, providing diversification benefits and reducing overall portfolio volatility. Certain private equity investments can also act as a hedge against inflation, preserving purchasing power over time.

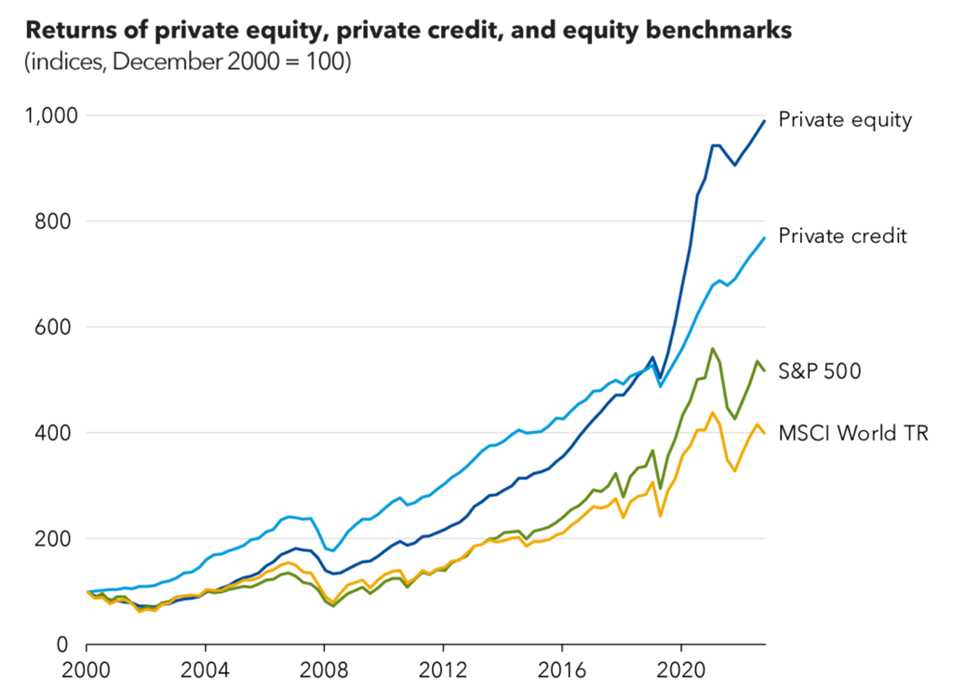

Private credit has delivered high returns with what appears to be relatively low volatility. The following chart illustrates the performance of different asset classes versus private credit (Source: Preqin and IMF)

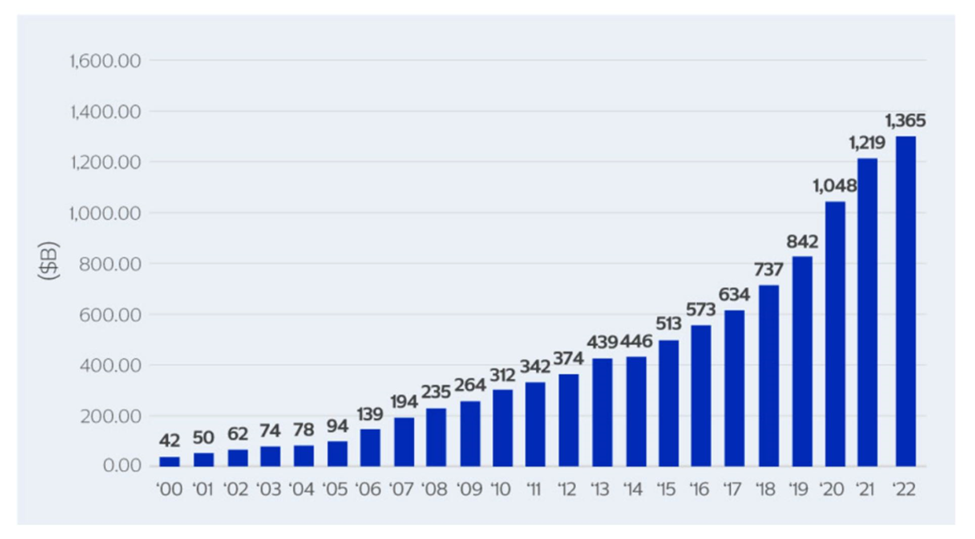

The private credit market has experienced significant growth in recent years due to investor demand for higher-yield investments. In 2024, the private credit market was estimated to be worth $1.5 trillion, up from $1 trillion in 2020. Projections suggest that this market will continue to expand, reaching $2.3 trillion by 2027 and $2.8 trillion by 2028. Morgan Stanley reports that private credit has seen substantial growth and could potentially become a $2.8 trillion market by 2028. In 2023, global private credit assets, which encompass private credit funds, business development companies, and private collateralized loan obligations, totaled approximately $2.1 trillion, with three-quarters of this amount originating from the United States. Businesses are increasingly relying on private lenders. To put this growth into perspective, the private credit market is growing at twice the rate of public markets. KKR states that private credit accounts for about 10% of the total debt for US non-financial corporations.

This alternative asset class offers attractive returns compared to traditional bonds and equities, but also comes with substantial risks. To mitigate these risks, diversification and shortening the duration of holdings are essential strategies.

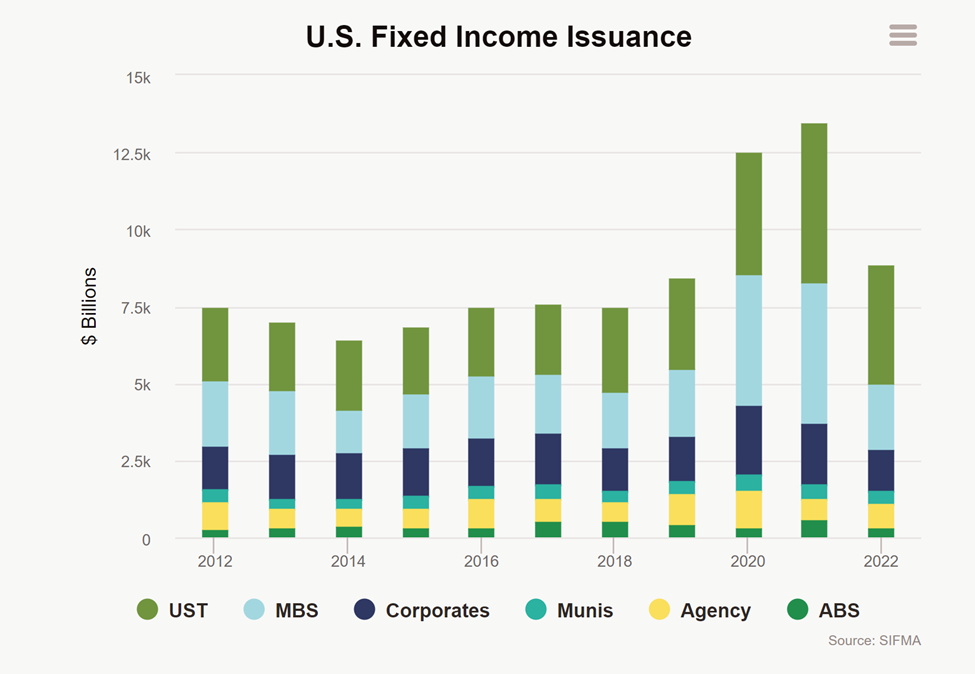

Investor demand for higher yields has played a significant role in driving the growth of the private credit market. Given the historically low interest rates, investors are now seeking alternative fixed-income instruments that can offer attractive returns. Private credit presents an appealing opportunity to generate substantial returns that can potentially outperform traditional bonds. Moreover, the stability and predictability of income streams provided by private credit make it an appealing choice for investors, especially when compared to the volatile equity markets. In 2022, the issuance of U.S. Treasury securities witnessed a notable decline of 25.5% from the previous year, amounting to $3.8 trillion. Long-term fixed income issuance experienced a significant YoY decrease of 34.2%, reaching $8.9 trillion. Mortgage-backed securities (MBS) issuance declined by 53.2% YoY, amounting to $2.1 trillion, while corporate bonds fell by 31.0% YoY, totaling $1.4 trillion. Additionally, U.S. long-term municipal bond issuance decreased by 19.2% YoY to $390.8 billion, while asset-backed securities issuance volume dropped by 48.0% YoY to $302.8 billion. On the other hand, federal agency securities demonstrated growth, increasing by 19.9% YoY, reaching $830.9 billion (source: sifma.org/resources/research/fact-book/).

Market Expansion has also contributed to the growth of the private credit market. Institutional investors such as pension funds, insurance companies, and endowments have increasingly allocated funds to private credit in order to enhance the yield of their portfolios. Additionally, the private credit market offers various investment opportunities, including direct lending, mezzanine debt, distressed debt, and specialty finance, which provide multiple avenues for generating yield. Private funds and securities offerings have gained mainstream prominence, with private securities offerings surpassing public securities offerings in recent years, reaching a ratio of approximately 4:1 between July 1, 2021, and June 30, 2022.

Investors have entered the market seeking investment returns and diversification, resulting in an expansion of the market’s size and significance. For instance, CalPERS, the largest U.S. public pension plan with approximately $500 billion in assets under management, announced in March 2024 its intention to increase its total private market allocation from 33% to 40% of plan assets and its private credit allocation from 5% to 8%. According to CalPERS’s performance review, private credit emerged as its highest-performing private asset segment, delivering a 13.3% annual return. Meanwhile, several public fund managers, including Franklin Templeton, have shifted their focus to alternative investments by acquiring private credit managers. Additionally, existing private credit managers, like Oaktree Capital Management, have expanded the size of their private credit funds. (Source: crsreports.congress.gov/product/pdf/IF/IF12642)

However, it is crucial to take into account the risks associated with private credit. One major concern is credit risk, as lending to companies that may not qualify for traditional bank financing increases the possibility of borrower default. Moreover, private credit investments are generally illiquid, posing a challenge to exit positions rapidly without incurring substantial losses. Market and economic risks, such as economic downturns and regulatory changes, can also have an adverse impact on returns.

Mitigating these risks is of utmost importance, and investors can achieve this through diversification and duration management. Diversifying alternative investment portfolios across different asset classes, geographies, and sectors aids in spreading risk and reducing the impact of any single underperforming asset class. Furthermore, shortening the duration of private credit investments minimizes exposure to long-term market and credit risks, providing greater flexibility to respond to changing market conditions and enhancing liquidity.

To conclude, the current growth of the private credit market reflects investors’ desire for higher-yield investments. While private credit offers attractive returns, proper management and diversification are crucial for effectively mitigating risks. Optimal outcomes and protection against potential downsides can be achieved by diversifying alternative investment portfolios and reducing the duration of holdings. When utilized effectively, private credit and private equity can be valuable components of a well-diversified investment portfolio.

#PrivateCredit #AlternativeInvestments #Diversification #RiskManagement #InvestmentPortfolio